Arizona Foreclosure Attorney

Stop A Foreclosure in Arizona

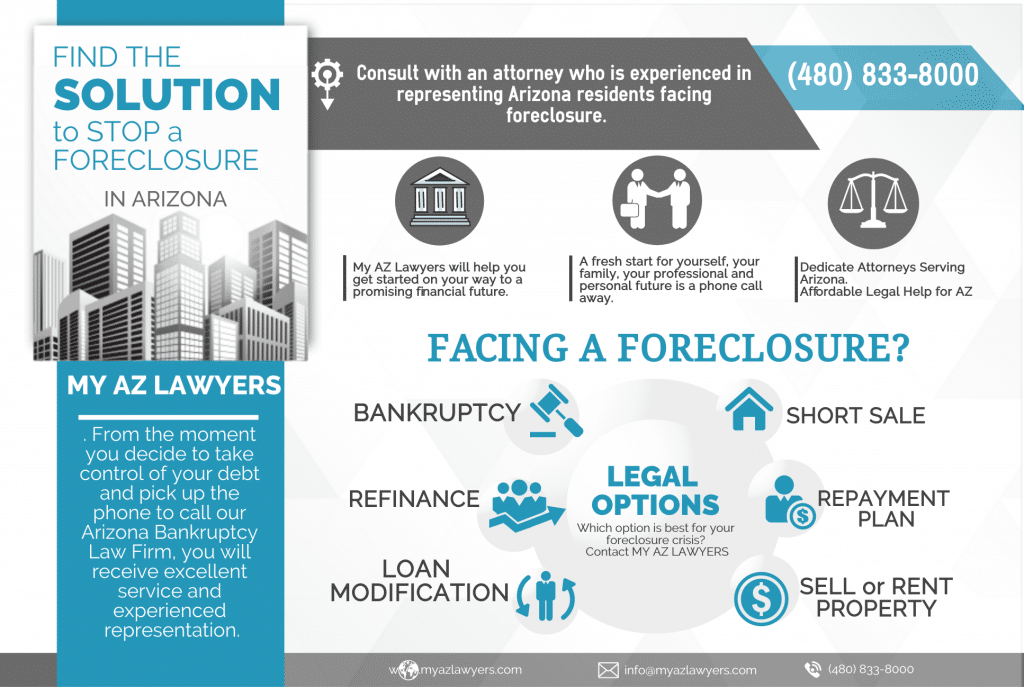

Facing a Foreclosure? What are Your Options?

My AZ Lawyers experienced attorneys can assist you if you are faced with a lender aggressively pursuing a foreclosure. Our debt relief experts can help you to understand your options and provide you with the best defense and representation to fight a foreclosure.

Each foreclosure case is unique. Our lawyers can offer solutions for your particular circumstances and foreclosure situation. What method of debt relief is the most beneficial to your case? Some solutions include a short sale or deed instead of foreclosure. Another option is filing for bankruptcy protection.

Filing for bankruptcy protection is one way to save your house from foreclosure. If keeping your home is your top priority, My AZ Lawyers debt relief team can help you understand the law. Armed with an experienced attorney and the information you need to make the best decisions for your situation, you will be able to successfully resolve your financial crisis.

ARIZONA FORECLOSURE FAQs

ANSWER:

Foreclosure is the process home loan lenders will take when borrowers miss too many of their mortgage payments. When a home is foreclosed, the lender will regain possession of the home and sell it at an auction. The sale proceeds will be contributed towards the balance of the loan. Any remaining balance after the sale is referred to as a deficiency balance, but some states by law do not allow for deficiency balances.

ANSWER:

The length of a foreclosure will depend on a number of factors like the applicable state’s laws, the lender’s practices, if the borrower attempts to negotiate alternative arrangements with the lender, etc. The average time it takes for a foreclosure to occur is 6-12 months.

ANSWER:

This, of course, will come down to a matter of personal preference. There is a social stigma against filing bankruptcy, so many feel too embarrassed to file. However, losing a home to foreclosure can be just as embarrassing. Filing bankruptcy can have a negative impact on your credit, but foreclosure will as well, and can make qualifying for loans in the future far more difficult. Bankruptcy may help you save your home, and will eliminate other debts in the process.

ANSWER:

The moment you file a bankruptcy protection, you will be protected by a bankruptcy procedure called the Automatic Stay. The Automatic Stay stops garnishments, repossessions, and most importantly, home foreclosures. The Stay lasts until the case ends, either through discharge or dismissal. The home foreclosure will resume after the bankruptcy is closed if the past-due balance isn’t settled during the bankruptcy.

ANSWER:

Yes. An Emergency Bankruptcy Filing, also known as a Skeleton Petition, is a shorter version of a bankruptcy petition that filers can use when they are in an emergency situation, such as a home foreclosure. The filer will only be required to present information about their income and their identification to start the protections of the Automatic Stay, and will have a deadline of two weeks to submit the rest of their bankruptcy petition. As long as the filer complies with that deadline, the foreclosure will be stopped or delayed by the Automatic Stay, depending on which chapter they file.

ANSWER:

Chapter 7 Bankruptcy typically lasts about 3-5 months from the date of filing. While unsecured debts like credit cards and medical bills will be discharged without the filer being required to repay anything, the unpaid balance on their mortgage will not be discharged. The filer will be protected by the Automatic Stay and will have the opportunity to try to pay the balance during the 3-5 month course of their bankruptcy. If they are unable to do so, the lender may proceed with foreclosure once the case is discharged (or dismissed). How quickly the lender will proceed with foreclosure will depend on the lender’s practices and how far behind the borrower is on payments.

ANSWER:

If you want to permanently stop a foreclosure, as opposed to temporarily delaying it, Chapter 13 will likely be your better option. Chapter 7 will not discharge the past-due balance on your mortgage that must be repaid to stop the foreclosure. Chapter 13, on the other hand, includes this past-due balance into your payment plan. Instead of having to pay that balance in a lump-sum payment, Chapter 13 filers will have their arrearages spread out into monthly payments that will last 3-5 years, depending on their income level. Once the Chapter 13 Bankruptcy payment plan is completed, debts will be discharged and the filer will be safe from home foreclosure.

ANSWER:

A home foreclosure will have a large negative impact on your credit, and will remain on your credit for 7 years. The decrease in your credit score will depend on your score before the foreclosure, but on average will decrease a credit score by about 100 points. This will make it difficult to qualify for new lines of credit, and almost impossible to qualify for a new home mortgage.

Chapter 13 will have less of a negative impact on credit than a Chapter 7 since debts are repaid in a Chapter 13. The impact of both chapters of bankruptcy will depend on the filer’s original score. However, filers with poor credit may even see a slight increase in their score upon filing. Another difference between foreclosure and bankruptcy is that there are many steps you can take after bankruptcy to rebuild your credit, like financing a vehicle or opening a secured credit card. A Chapter 7 bankruptcy will remain on your credit for 10 years from the date of filing, and a Chapter 13 will remain on your credit for 7 years from the date of filing. Filers will be eligible for a home loan 2 years from the date of filing.

Arizona Homeowners facing Foreclosure

Many individuals in Arizona have felt the effect of a dismal housing market in Phoenix, Mesa, Gilbert, and Chandler. When unable to make monthly mortgage payments, a lender may take swift legal action to collect the debt. If you feel you are falling behind on house payments and cannot seem to get ahead, or if you are facing a foreclosure, you are not alone. Don’t lose hope. Instead, seek the help of an Arizona foreclosure attorney who will evaluate your case and get you back on track. If your credit isn’t good, if you are feeling that a foreclosure is looming and you want to take control of the situation, you have options that will help you navigate the foreclosure process.

Options to Avoid a Foreclosure

Choosing to work with a debt relief expert at My AZ Lawyers will make a significant difference if you need to avoid a foreclosure. Our law firm has a reputation for successfully helping Arizona residents facing foreclosure. The team of professionals at our law firm will discuss your options and use their experience and expertise in Arizona Bankruptcy Law to help you stop a foreclosure.

Listed below are some options that may help:

• Short Sale

A popular option used for avoiding a home foreclosure, short sale will allow you to get out of your mortgage crisis and limit the damage to your credit rating. After a short sale process, you may be able to apply for a new loan in 24 months. If a home is foreclosed, you may not be able to take out a loan for five to seven years. To be eligible for short sale, you must prove financial hardship, the amount of debt is more than the market value of your investment, and your monthly income is less than your expenses. Contact My AZ Lawyers if you have further questions about how a short sale works in Arizona.

• Filing for bankruptcy

Filing bankruptcy in Arizona is an option to stop foreclosure, but proceed with the legal advice of an attorney. Consider this solution if you have other debts as well as a mortgage.

• Mortgage Modification

A lender sometimes will allow a modification. This means you wish to change mortgage so that the payments will be more manageable for you. The modification would be subject to the approval of the lender, and may not change the fact that the total loan is still underwater.

• Reinstatement

Possibly a difficult option if you currently cannot keep up with payments, but a reinstatement includes paying the debt amount with late fees to the lender after the due date. This would allow the mortgage to be reinstated until the foreclosure.

• Rent your house

If you can rent your home for the amount of money to cover the mortgage payment, you could consider renting your property. If repairs are needed to achieve this, think about how the cost to repair may exceed the benefit of renting for a needed price per month. Obviously, if you are not willing to be in a landlord position, this option may not be suitable for your needs.

• Repayment Plan

A repayment plan can help you stop a foreclosure in Arizona because the lender allows you to catch up on missed payments over a period of time. You repay the lender along with the current mortgage payments. A lender needs to approve of this option.

• Sell your property

Maybe it would be in your best interest to sell the property if you have enough equity left. This would not be the best option if you owe ore than the current value of the property.

• Refinance

Arizona law does allow you to apply for a loan to repay a mortgage. You must meed eligibility requirements for a new loan. It may be difficult to get a refinance if you have a record of missed loan payments.

• Deed-in-Lieu of Foreclosure

Deed-in-lieu needs the approval of the lender before beginning the process. Deed-in-Lieu of foreclosure allows you to vacate the property and return the property to the lender. This may still have a great impact on your credit rating and make it difficult to get a future loan.

The most important thing to understand if you are facing foreclosure is to consult with an expert Arizona foreclosure attorney. With all the options available, finding the best means to a successful financial future is an important priority. My AZ Lawyers have helped homeowners in Arizona faced with foreclosure, and our firm can give you professional, experienced representation you need.